Article Originally posted on Fairview Lending

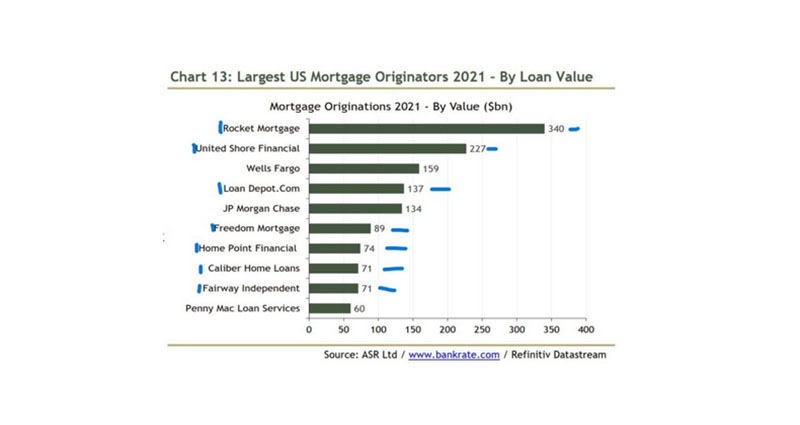

The federal government in their quest to shore up the mortgage market in 2008 has created some new risks to the housing market. Non bank lenders now make up 74% of the origination volume with only 3 banks even making the list. What does this mean for the mortgage market and in turn the housing market? Why are non bank lenders now making up such a large share of originations? Do we have another large scale “wreck” coming our way?

Why are non bank lenders gobbling market share from traditional banks?

Before talking about why banks are gaining market share, it is important to discuss Dodd Frank. The response to the 2008 mortgage crisis was the creation of increased regulation in banks to prevent future crashes. What was in Dodd Frank?

Dodd Frank is a series of measures that first required banks to have more capital on hand, meaning more of their own money would be at risk when they lend, and second, a set of measures restricting certain kinds of lending activities, in particular, nontransparent chopping and dicing of loans into other securities. And a third piece of the action, particularly aimed at the too-big-to-fail institutions, is that they were forced to create what are called ‘living wills,’ which are supposed to make it easier for authorities to unwind or shut down a troubled financial institution when a crisis hits.

“The fourth, and in some ways perhaps most important, was that the largest institutions, not just in the U.S. but throughout the advanced economies, are now subject to what are called stress tests. Stress tests are a specific form of simulation developed by the Federal Reserve and other central banks to allow them to figure out how badly a given financial institution’s portfolio would hold up if there was a broad sell-off across a bunch of asset classes, or a specific kind of shock like what we suffered in 2008.

Non Bank lenders not bound by Dodd Frank

Unfortunately, the way Dodd Frank was written there is a huge loophole. If you look at the list above, only the bank lenders are bound by Dodd Frank. The other lenders do not have to follow the same regulations with Capital requirements, stress tests, etc… which has led to their huge gains in market share. Without the regulatory burden, non-bank lenders can typically provide loans cheaper than many of their bank counterparts which has led to them gobbling up 74% of the mortgage market.

Why is it “riskier” for non bank lenders to play such a large role in the mortgage market?

- Don’t have the balance sheets of big banks: There is no capital requirement so when things go south in the mortgage market, there are not assets to back things up.

- Don’t have the loan diversification of traditional lenders: Take a lender like Rocket Mortgage, they are focused on the residential market, as the residential market tanks so does their business model. Banks on the other hand have various business lines/loans to diversify their income

- Revenue relies on new originations: Non bank lenders rely heavily on new originations for their revenue as opposed to a bank that has various revenue sources.

What is causing a possible wreck in the mortgage market to happen?

Rising rates have stopped the refinance market and drastically slowed purchase volumes. Remember bond prices move in inverse to rates so the higher the rate, the lower the bond price. Rising rates are pushing down the value of their mortgage bond portfolio.

Furthermore, non-bank lenders do not have a diverse revenue stream nor the reserves banks have which could lead to a bad correction in the market. There could be a swift change in the real estate market as rates rise considerably faster than originally anticipated. Depending on how quickly this change occurs, many non bank lenders could be caught off guard with serious cash flow issues.

Furthermore, the market assumes that underwriting is tougher this time around than the last cycle, yet I am not convinced.

Average down payment not 20%, only 6%

Contrary to popular belief, the average down payment is not even close to 20%. The average American pays about 6% of the home price for their down payment, according to data from Attom Data Solutions.

How bad will this mortgage market wreck be?

We found out during the last cycle that the number one determination of default was equity. Unfortunately, 6% down does not give me much confidence that a wreck is not in the cards. Furthermore with non bank lenders with limited assets originating 74% of all loans, the ability for a mortgage meltdown is profound.

Most economists believe that the real estate market is in for a reset of 10-20%, this means a large swath of borrowers are immediately underwater and will likely default. Furthermore 74% of these loans were originated by non bank lenders that there will be limited assets to go after to recover losses.

What we saw in the last cycle is that many loans were originated that were not properly underwritten. What happens when a similar occurrence occurs in this market? Also, what happens when a non bank lender is unable to unload their originated loans for whatever reason? Both of these scenarios are real possibilities that could lead to a train wreck again in the mortgage market.

What does a wreck in the mortgage market mean for real estate values?

Every article states that we will not see a repeat of 2008. I would agree it will not be a carbon copy, but there still could be a blow up in the real estate market as a result of the mortgage market. As rates continue to rise, you will see mortgage rates easily crest 7% next year. Furthermore many of the non bank lenders will go out of business which will lead to less competition and ultimately even higher rates.

Summary

Although I’m not seeing 40% plus drop in prices in most markets today, the possibility does exist. Currently I am sticking with my previous prediction of a 10-20% reset in the prices in most markets, with some markets poised for even further drops.

The wild card is the mortgage wreck that we are about to witness where non bank lenders come under intense pressure. If a large-scale wreck in the mortgage market occurs, we could look much more like 08 with 20-30% declines in prices as lenders have to dump loan pools at huge discounts. Furthermore, my confidence in a soft landing is very low with the average down payment of 6%. Although we aren’t in store for a 2008 rerun, we are in for a 2022/23 reset in the real estate market. The only question is will we see a reset of 10% or 40% or somewhere in between.